# Stochastic Processes: Understanding Random Phenomena and Applications in Finance

## Introduction

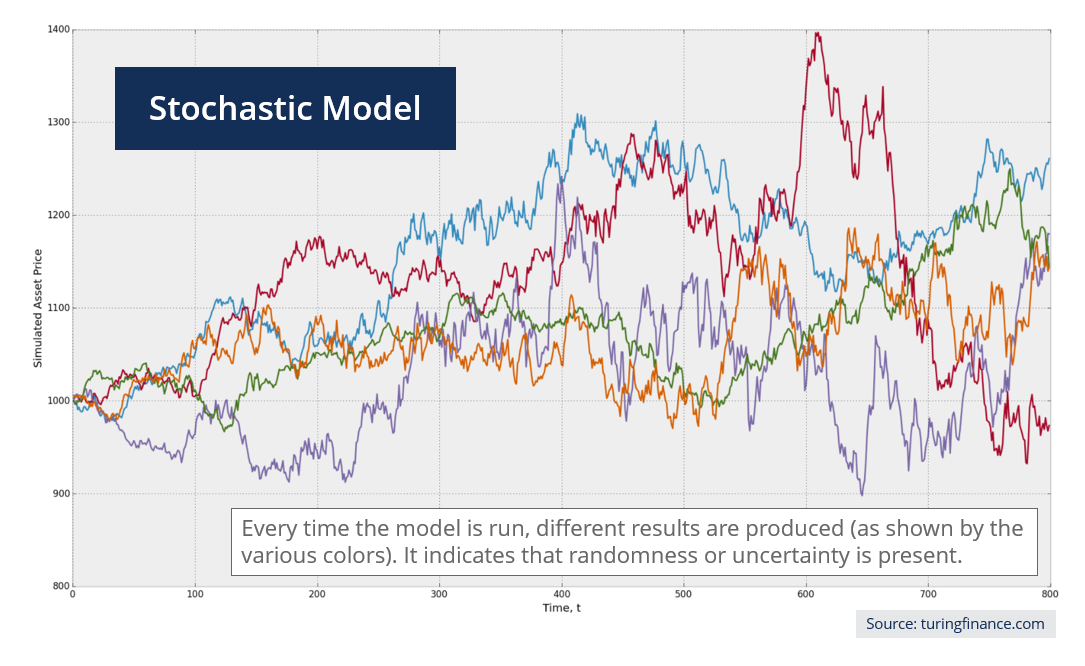

In *The Dao of Capital: Austrian Investing in a Distorted World*, Mark Spitznagel introduces various concepts related to stochastic processes in the context of finance and investing. In essence, a stochastic process models the evolution of a system that evolves over time in a random, unpredictable manner.

[](https://i.ytimg.com/vi/go0EY_cfdPs/maxresdefault.jpg)

*Example of Geometric Brownian Motion in finance.*

We focus on continuous-time stochastic processes, the backbone of many models in modern finance. One prominent example of a stochastic process is the Geometric Brownian Motion (GBM), central to the ever-popular Black-Scholes-Merton (BSM) model for option pricing.

## Core Concepts of Stochastic Processes

[](https://www.engineerstutor.com/wp-content/uploads/2018/10/1-2.jpg)

*Illustration of a random variable in experiments.*

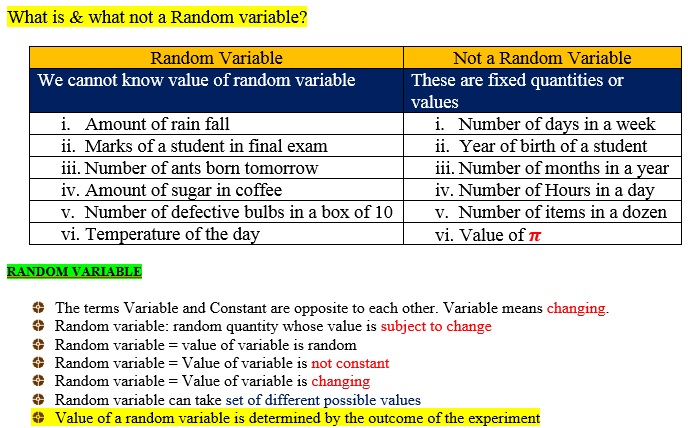

A stochastic process builds on the underlying concept of a *random variable*: given a random experiment (or *trial*), the outcome(s) of the trial(s) exhibit randomness captured by the notion of a random variable, which assigns a value, a *realization*, to each experiment (e.g., rolling a fair dice, the outcome is a value from 1 to 6).

Now, imagine a collection of random variables, each representing the outcome of a trial *indexed* (or *keyed*) by time, *t*, $X(\omega, t)$. This collection, denoted as $X(\omega, t)$, forms a stochastic process, with $\omega$ as the elementary event, the basic unit for expressing the outcomes of the random experiment.

As time evolves, $\omega$ generates multiple realizations of $X(\omega, t)$, or the *sample path*, offering the *time series* of the stochastic process. In other words, a stochastic process creates a universe of potential scenarios, inherently probabilistic in nature.

## Stochastic Processes and Financial Modeling

Incomplete knowledge about outcomes motivates the use of financial models based on stochastic processes. The core idea is modeling outcomes' range of possibilities via a distribution of returns (probabilities) and dependencies (correlations).

Financial modeling hinges on key features of stochastic processes: *paths* and *distributions*. Path-dependence implies the state at a time impacts the subsequent state; the distribution of returns, on the other hand, manifests the *randomness* of the returns.

[](https://cdn.corporatefinanceinstitute.com/assets/stochastic-modeling1.png)

*Diagram showing the application of stochastic processes in financial modeling.*

### Example 1: Black-Scholes-Merton Model

A cornerstone of financial mathematics, the BSM model for option pricing, relies heavily on GBM, a continuous-time stochastic process. The GBM assumes that returns follow a *lognormal distribution* and *path-independence*.

[](https://ds055uzetaobb.cloudfront.net/brioche/uploads/8gi1CwayJG-z-score-diagram.png?width=1200)

*Black-Scholes-Merton model equation.*

Suppose stocks follow GBM; then, stock prices, $S_t$, follow:

\[dS_t = rS_tdt + \sigma S_t dW_t\]

where $r$ is the risk-free interest rate, $\sigma$ is the stock's volatility, and $dW_t$ is the Wiener process (or Brownian motion), representing the randomness.

The intuition from the GBM equation is that stock prices fluctuate randomly: at each $t \rightarrow t+ \Delta t$, the stock price moves by a random $\epsilon_t$.

(Note: for simplicity, the GBM derivation assumes a risk-free interest rate $r$, constant with time, but more intricate models do exist, such as the Heston model, addressing the limitations of GBM).

### Example 2: Stochastic Volatility

To overcome GBM and BSM's unrealistic assumptions (e.g., constant volatility), stochastic volatility (SV) was posited, allowing volatility to be a function of the random Wiener process, distinct from the stock dynamics of GBM.

One widely used SV model is the Heston model. The Heston model captures the clustering of volatility: periods of high volatility will likely be followed by more volatility.

[](https://i.ytimg.com/vi/KncOcHnEA3Q/maxresdefault.jpg)

*Understanding the Heston model for stochastic volatility.*

In summary, we reiterate that stochastic processes constitute an essential pillar for financial modeling in a distorted world. By capturing the essential mechanics of stochastic processes, we can better understand the evolution of returns, volatility, and the cross-sectional relationship between stocks (and other assets), allowing for a more informed investment decision-making process.

## Conclusion

This overview of the stochastic processes underpinnings of financial modeling sheds light on the complexity inherent in understanding and optimally investing in capital markets.

As stated by Mark Spitznagel, the Dao of Capital lies in an acute understanding of risk and volatility embedded within financial markets. Stochastic processes offer a lens through which to analyze risk and volatility, and by doing so, one may begin to appreciate the intricacies of financial markets.

To deepen students' understanding of stochastic processes' bearing on finance, I suggest the following further explorations:

- Investigate alternative Stochastic Volatility models (SV): the SABR model

- Delve into models for stochastic interest rates, e.g., Cox-Ingersoll-Ross (CIR) model and Hull-White model

- Examine other applications of stochastic processes in finance: Real options, risk management, derivatives pricing

Embracing stochastic processes and the associated stochastic calculus is the first step in enriching our understanding of financial turbulence; it is prudent for our journey towards mastering the Dao of Capital.

Last updated: 2024-12-05

Related Books

Related Knowledges