# Asymmetric Information: Unraveling the Hidden Dynamics of Risk and Decision-making

In the realm of decision-making and risk management, there exists a powerful yet often underappreciated concept: asymmetric information. At its core, asymmetric information refers to a scenario where different parties have access to different quantities and qualities of information. This concept is so integral to our understanding of rational choices, market dynamics, and policy formulation that economist George Akerlof, along with Michael Spence and Joseph Stiglitz, was awarded the Nobel Prize in Economic Sciences for his work on asymmetric information and imperfect markets in 2001.

[](https://www.millenniumpost.in/h-upload/2021/08/21/580983-4054trxub1bo3seewpstcvijvauzpengmmt05472888.jpg)

*The Nobel Prize in Economic Sciences*

Asymmetric information plays a critical role in Nassim Nicholas Taleb's book *Antifragile*, where it sheds light on the deep complexities inherent in systems and decision-making processes. In this context, a thorough understanding of asymmetric information can help us distinguish between fragile, robust, and antifragile systems, allowing us to make wiser decisions in the face of uncertainty.

In what follows, we dive into the intricacies of asymmetric information, illustrating its applications and manifestations with concrete, practical examples. We will examine the implications of asymmetric information in several domains, namely insurance, financial markets, and labor markets, to reveal the hidden risks and opportunities that lie beneath the surface.

## Insurance: A Playground for Asymmetric Information

The insurance sector offers a rich ground for understanding the dynamics of asymmetric information. At its heart, insurers gather premiums from a large pool of policyholders and subsequently distribute the aggregate sum among the fraction of clients who incur losses during a specific period. This arrangement can produce asymmetric information if insurers find it challenging to distinguish between low-risk and high-risk clients adequately.

Adverse Selection (Hidden Information)

A classic example of asymmetric information occurs when a policyholder holds back crucial information about their risk profile to secure a more favorable insurance contract. In this case, when an individual has a better understanding of their health condition than the insurer, this is known as adverse selection due to hidden information.

[](https://www.investopedia.com/thmb/GbW_aqRMX9NF-_17BSsI7nqlGQo=/1500x0/filters:no_upscale%28%29:max_bytes%28150000%29:strip_icc%28%29/adverseselection.asp-FINAL-c205497ee83c44358ad2e1a403cc4719.png)

*Adverse Selection in Insurance*

Consider a life insurance scenario where an individual is aware that they have a hereditary medical condition and have a higher likelihood of succumbing to a certain disease than the general population. By withholding this critical detail, the person might receive a lower premium than they would if the insurer were privy to their medical condition. If the prevalence of adverse selection is substantial, it can adversely impact the insurer's profitability and destabilize the insurance market.

Moral Hazard (Hidden Actions)

Another exemplification of asymmetric information in insurance pertains to 'hidden actions' or moral hazard, where the policyholder alters their behavior after securing insurance coverage. As the insured party has superior knowledge of their post-contract behavior, this can engender moral hazard. For instance, an individual who purchases theft insurance may become careless in safeguarding their belongings, thus increasing the likelihood of theft.

[](https://www.investopedia.com/thmb/uL_LWzyQvFdbSDX9VB9db-j3CAQ=/1500x0/filters:no_upscale%28%29:max_bytes%28150000%29:strip_icc%28%29/moralhazard-final-e071d0d67fc0429896cf95f25e915b85.jpg)

*Moral Hazard Example*

The example of automobile insurance further illustrates the concept of moral hazard. Upon securing car insurance, many drivers may indulge in riskier driving habits, given that their potential losses are effectively shifted to the insurer. In response to these adverse incentives, insurers often implement deductibles, policy limitations, and monitoring systems to minimize moral hazard risk.

## Asymmetric Information in Financial Markets: The Hidden Risks Behind the Curtain

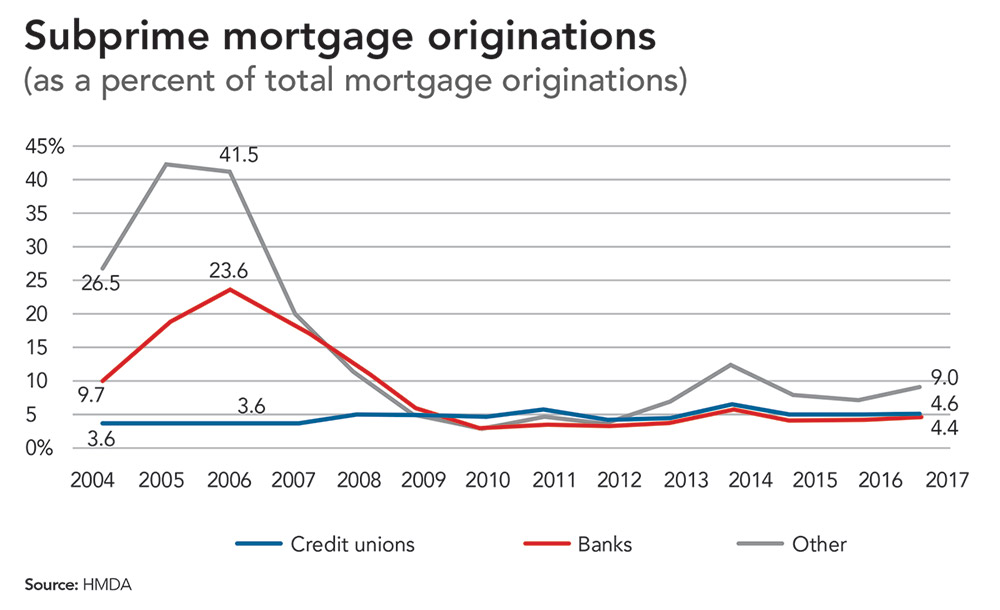

The labyrinthine dynamics of financial markets can mask significant information disparities among market participants, leading to a wide range of consequences from boosting transaction costs to engendering systemic risk. The subprime mortgage crisis of 2008-2009 is an exemplary case where asymmetric information, coupled with complex financial products and misaligned incentives, played a significant role in triggering a global financial crisis.

Widespread use of securitization tools, such as mortgage-backed securities (MBS) and collateralized debt obligations (CDOs), allowed major financial institutions to repackage and distribute mortgage loans as investments to global investors. However, these packages often contained subprime mortgages with high default risks, but the intricacy of these products masked the actual risk levels associated with these financial instruments. As a result, investors—including other financial institutions—mispriced and overexposed themselves to these assets, leading to a chain reaction of defaults and a crisis of confidence that ultimately precipitated a financial maelstrom.

[](https://news.cuna.org/ext/resources/Online/2019/09/09-23-19_subprime-mortgage-originations.jpg)

*Subprime Mortgage Crisis*

## Asymmetric Information in Labor Markets: The Wage Gap and the Power of Bargaining

The influence of asymmetric information extends beyond insurance and financial markets, seeping into the very bones of labor markets. A key domain of labor market asymmetry encompasses the wage gap and the bargaining power imbalance between employers and employees.

Information asymmetry can exacerbate this issue through a lack of transparency in pay scales and remuneration packages. In many instances, job seekers are not privy to the exact wage levels of their peers, making it difficult for them to discern whether they are receiving fair compensation for their work. This opacity can leave employees vulnerable to accepting lower wages than they would otherwise negotiate if armed with the requisite knowledge.

[](https://iwpr.org/wp-content/uploads/2020/08/Screen-Shot-2020-08-16-at-1.56.54-PM.png)

*Wage Gap and Bargaining Power*

The wage gap's manifestation varies across different industries, but identifying and addressing information disparities can empower employees to negotiate more favorable terms and promote equity in the labor market.

## Conclusion and Pathways to Further Exploration

As we have traversed the sprawling landscapes of asymmetric information, it becomes evident that this concept casts long shadows over various domains, such as insurance, financial markets, and labor markets. Thoroughly understanding and internalizing the intricacies and ramifications of asymmetric information constitute crucial components of prudent risk management and decision-making, particularly in an ever-evolving and unpredictable world.

As a next step in deepening your appreciation of asymmetric information, consider reading works by other eminent scholars such as Michael Spence and Joseph Stiglitz, who, alongside George Akerlof, were instrumental in shaping our modern understanding of information asymmetries and their consequences. Additionally, further investigating topics such as agency theory and information economics can illuminate the interwoven complexities of decision-making, risk management, and organizational structures.

By cultivating a deep comprehension of asymmetric information, you will not only be better equipped to decipher the risks and uncertainties lurking beneath the surface but also to augment your ability to formulate effective strategies to mitigate these complexities. Ultimately, this enhanced proficiency will position you to navigate the labyrinthine realms of risk, decision-making, and organizational dynamics with acumen and sagacity.

Last updated: 2024-04-10

Related Books

Related Knowledges